CDD stands for Community Development District, and despite what many people think, it isn’t simply “another tax.” A CDD is a special financing district created to fund the infrastructure and amenities that make a neighborhood attractive and functional. Think roads, sidewalks, lakes, parks, clubhouses, pools, fitness centers, landscaping, and even utility systems. Instead of requiring the developer to build all of these improvements into the home’s purchase price, the cost is spread over time among the homeowners who benefit from them. Understanding what a CDD actually pays for can completely change how you evaluate the true cost and value of a home.

CDD stands for Community Development District, and despite what many people think, it isn’t simply “another tax.” A CDD is a special financing district created to fund the infrastructure and amenities that make a neighborhood attractive and functional. Think roads, sidewalks, lakes, parks, clubhouses, pools, fitness centers, landscaping, and even utility systems. Instead of requiring the developer to build all of these improvements into the home’s purchase price, the cost is spread over time among the homeowners who benefit from them. Understanding what a CDD actually pays for can completely change how you evaluate the true cost and value of a home.

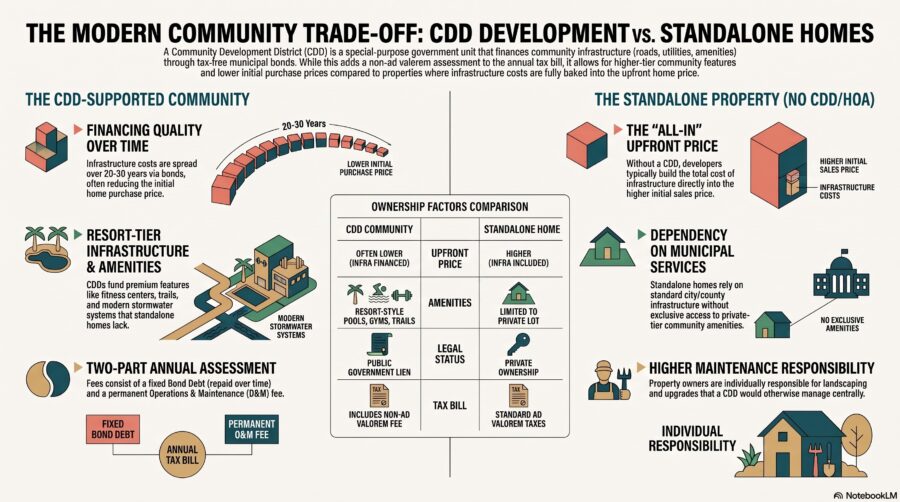

Let’s see what the pro’s and con’s are.

- You’re financing infrastructure over time

Instead of paying thousands or tens of thousands of dollars more in the purchase price, the developer finances roads, utilities, drainage, clubhouses, pools, parks, sidewalks, and landscaping through the CDD.

Think of it this way:

- Community A: Home price $650,000, no CDD

- Community B: Home price $615,000 with a $2,500 annual CDD

You finance less mortgage and pay the infrastructure separately over many years. Depending on interest rates, down payment, and how long you own the home, this can sometimes improve affordability.

- You’re paying for amenities you actually use

Many CDD communities include:

- Resort-style pools

- Fitness centers

- Tennis and pickleball

- Walking trails

- Dog parks

- Playground areas

- Beautiful landscaping

- Wider roads

- Better stormwater systems

Without a CDD, those amenities may simply not exist.

The question becomes:

Would you rather pay a little every year and enjoy these amenities every day, or save the fee and not have them at all?

- Newer infrastructure means fewer surprises

Most CDD communities are newer developments.

That usually means newer:

- Roads

- Sidewalks

- Water and sewer systems

- Storm drainage

- Street lighting

- Parks

Older communities without CDDs often face aging infrastructure that may eventually require special assessments, higher taxes, or HOA increases.

A CDD doesn’t eliminate future costs, but it often means the community started with modern infrastructure funded through a planned financing mechanism.

- Sometimes the HOA is actually lower

Many buyers assume:

“No CDD = cheaper.”

Not always.

Some communities without a CDD have significantly higher HOA dues because the HOA is responsible for maintaining amenities and infrastructure that a CDD would otherwise fund.

You have to compare:

- Mortgage

- Property taxes

- HOA

- CDD

- Insurance

The monthly total matters more than any single line item.

- CDDs usually have an end date

Many CDD bonds are issued for 20 to 30 years.

Once the bonds are paid off:

- the debt portion often ends,

- although there may still be an operations and maintenance assessment.

Many buyers don’t realize they’re not necessarily paying the same amount forever.

- Better-maintained neighborhoods can support resale value

While there are no guarantees, consistently maintained:

- landscaping,

- recreation facilities,

- roads,

- entrances,

- common areas,

can make neighborhoods more attractive to future buyers.

You’re not just paying for today’s appearance. You’re helping preserve the community’s appeal over time.

- Everyone shares the cost

Instead of the original developer bearing all infrastructure costs and building them into the sales price, the cost is spread among everyone who benefits from living there over many years.

Many buyers prefer this because they don’t have to finance the entire infrastructure cost in their mortgage on day one.

The counterpoint you should acknowledge

There are perfectly valid reasons someone may want to avoid a CDD:

- They plan to stay only a few years.

- They don’t use the amenities.

- They prefer established neighborhoods.

- They’re focused on minimizing annual carrying costs.

- They have a fixed retirement income.

Those are legitimate preferences, and it’s important not to dismiss them.