When Florida retiree Sue Maher received her renewal notice in late 2024, the “Paradise Tax” hit like a Category 5 surge. Her premium, already a staggering $3,800, jumped by an additional $2,000. For years, this was the Florida standard: a “hot mess” market where premiums tripled the national average and carriers fled the state like tourists ahead of a tropical storm.

When Florida retiree Sue Maher received her renewal notice in late 2024, the “Paradise Tax” hit like a Category 5 surge. Her premium, already a staggering $3,800, jumped by an additional $2,000. For years, this was the Florida standard: a “hot mess” market where premiums tripled the national average and carriers fled the state like tourists ahead of a tropical storm.

But as we move through 2026, the script has flipped. A combination of aggressive state intervention, a massive influx of private competition, and the technical revelations of the 2024 Residential Wind-Loss Mitigation Study has created a rare window of opportunity. If you are still paying 2023 rates, you aren’t just a victim of the climate; you’re a victim of a legacy actuarial shell game.

Here is how the smartest homeowners are clawing back their cash in this new market.

The High Cost of a Single Nail: The “Clip” Secret

In the world of insurance math, there is a massive gulf between a “toenail” and a “hurricane clip.” Most older Florida homes have their roof trusses attached to the walls using metal straps. However, if those straps are only secured with two nails, the industry classifies them as “toenails”—essentially just nails driven at an angle through the wood.

By simply adding a third nail through the metal strap into the truss, you move your home into the “hurricane clip” category. This isn’t just a minor repair; it’s an actuarial reset.

The Bottom Line for Your Wallet: This single nail changes your “loss relativity”—the multiplier insurers use to weigh your home’s risk against a baseline structure. According to the 2024 Study and data from carriers like Kin, this upgrade can slash the hurricane portion of your premium by up to 50%.

“This minor difference has dramatic effects on your insurance costs because it moves the straps from being categorized as toenails to hurricane clips. Having clips can save you up to 50% on the hurricane portion of your home insurance premium.” — Kin Editorial Staff

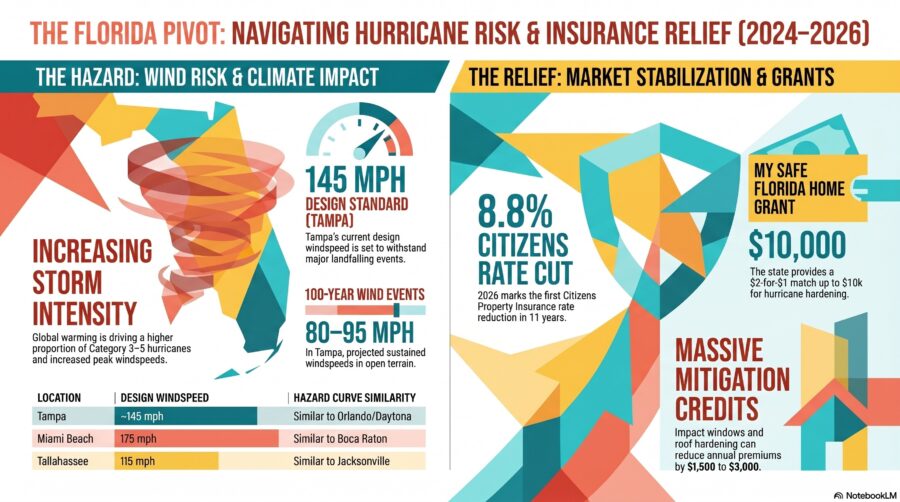

The $10,000 “Check in the Mail”: Why You Must Act Now

The “My Safe Florida Home” program has become the state’s most powerful weapon against the insurance crisis, offering a 2-for-1 matching grant. If you invest $5,000 in hardening your home, the state hands you $10,000.

However, as an advocate, I must warn you: this is a sprint, not a marathon. In 2024, the state burned through $200 million in just two weeks, leaving 45,000 homeowners stranded on a waiting list. The 2025-2026 cycle opened with $280 million in August, and the money is moving fast.

The Insider Eligibility Check:

- Income: Limited to low/moderate-income households (at or below 120% of county median).

- Permit Date: Your home’s building permit must pre-date January 1, 2008.

- Value: The home must be primary (homesteaded) and insured for $700,000 or less.

The “Quiet Flip”: Why Citizens Is No Longer the Safe Bet

For years, Citizens Property Insurance was the “insurer of last resort” that everyone wanted. In 2026, the roles have reversed. Thanks to 2022’s tort reforms and a softening global reinsurance market, 17 new private carriers—including names like Tailrow and Viceroy—have flooded the state.

These private companies are now doing the unthinkable: undercutting Citizens. This is due to the “Glide Path” law, which prevents Citizens from raising or lowering rates beyond a set percentage each year. While Citizens is legally tethered to its slow-moving math, private carriers are filing for aggressive rate decreases.

2026 Citizens Average Rate Reductions:

- Broward County: 14.1%

- Miami-Dade County: 14.0%

- Palm Beach County: 11.9%

- Statewide Average: 8.8%

The 120-Day Gift: If you receive a non-renewal notice, do not panic. Florida law now requires a 120-day notice. This 4-month window is a gift. Use it to shop the new private market; in 2026, staying with the “default” option is the fastest way to overpay.

The Invisible Vulnerability: Beyond the Roof

The 2024 ARA Study has shifted the focus from “will the roof blow off?” to “how much water gets in?” Modern insurance modeling now targets “envelope failures.”

A major revelation in the study is the vulnerability of sliding glass door tracks and soffits. When a vinyl or aluminum soffit fails, it doesn’t just let in rain; it allows the attic to pressurize. This “internal pressurization” pushes outward on the roof and walls, effectively doubling the wind load on your home’s structure.

The Industry Secret: Insurers are beginning to reward the installation of secondary water barriers and reinforced door tracks. Even if your roof holds, a failure in these “invisible” areas can lead to a total interior loss, which is why 2026 modeling is obsessed with floor-track integrity.

The $3,000 Dividend and the “Roof Aging” Trap

Impact windows remain the gold standard for opening protection, often yielding annual premium dividends between $1,500 and $3,000. This is your only real hedge against the “Hurricane Tax”—the legal right of the state to assess all policyholders (even private ones) if Citizens’ reserves are depleted after a storm.

However, be warned: the 2024 ARA Study introduced a “Roof Cover Aging” variable. If your asphalt shingles are over 15 years old, insurers may negate your window credits. The modeling now accounts for the brittleness of aging shingles, meaning a “hardened” home with an old roof is still a high-risk asset in the eyes of an underwriter.

The Price of Paradise: While the market is stabilizing, your rights have taken a hit. The elimination of one-way attorney fees was the trade-off for these lower rates.

“Three years from now it damn well better [lower costs], because it eviscerated consumer rights. The economic risk of suing an insurance company going forward is so high that you have to be willing to lose money.” — Amy Bach, Executive Director of United Policyholders

Conclusion: A Game of Inches

The Florida market has transitioned from a chaotic “hot mess” to a technical “game of inches.” Your premium is no longer just a factor of your zip code; it is a reflection of your latest wind-mitigation inspection.

If you are operating on an inspection from 2020, you are likely subsidizing your neighbor’s lower rates. In 2026, the data is clear: the market is finally rewarding homeowners who harden their structures and shop their policies.

In 2026, the most expensive mistake a Florida homeowner can make is not shopping their policy or ignoring the power of a third nail.